These supplementary statistics will now only be produced each quarter rather than monthly as they take a long time to prepare and the trends tend to be too slow moving to show any significant movement on a monthly basis.

Segment Performance

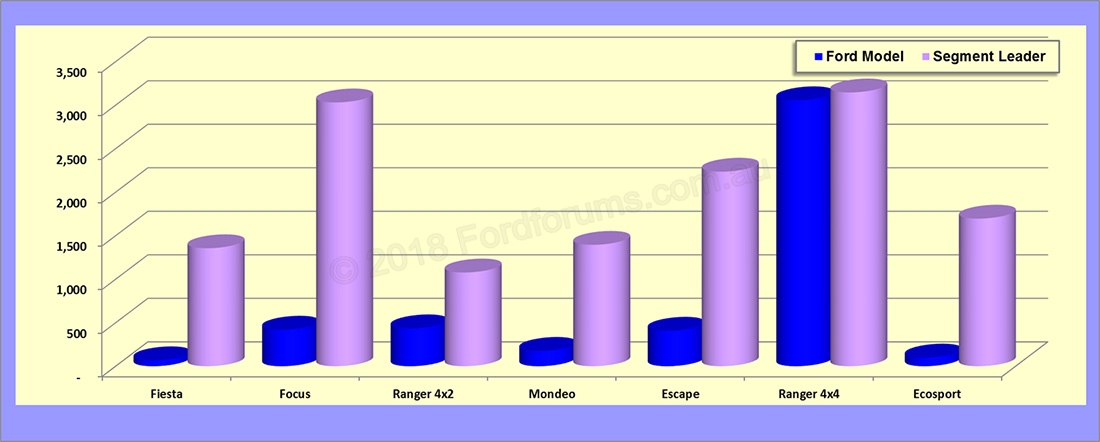

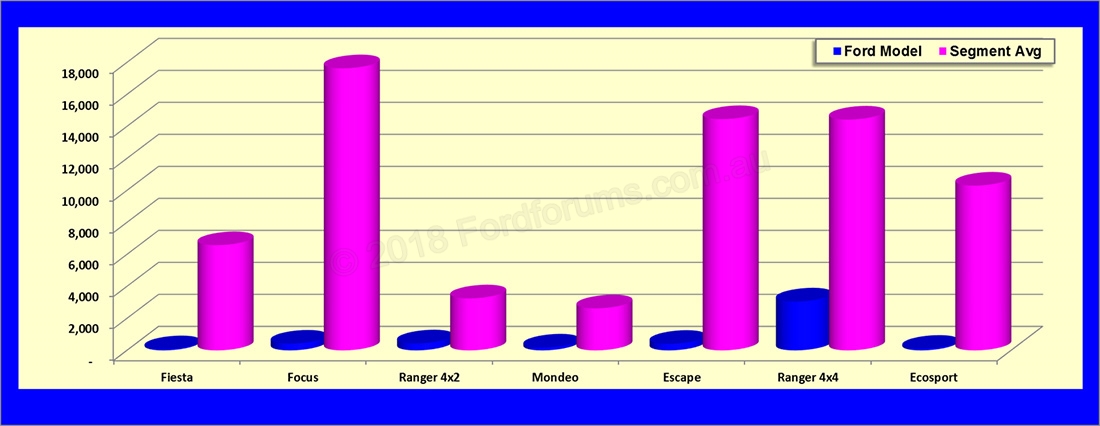

The first couple of charts are a graphical representation of the respective Ford models against the segment leader and the average sales for the segment over the last (rolling) 12 months so that in a volatile market the figures provided have relevance in determining trends.

From these we can see:

- the Ranger 4x2 is losing ground with 2.47:1 and the monthly average now down to 436;

- Focus (7.21:1) and Fiesta (19.84:1) are a long way off the mark with ever increasing gaps;

- Mondeo (7.9:1) is also a long way off the mark but the numbers are improving;

- Escape, with a 408 per month average is being outsold 5.48:1 by the class leading CX5 and the gap is widening;

- Ecosport is being outsold 17:1 by the class leading Mitsubishi ASX and the numbers are getting worse; and

- Ranger 4x4 is being outsold 1.03:1 by the class leading Hilux 4x4.

Note that as these are averages over the entire 12 months the impact of sales changes is amortised across that time frame and thus not immediately visible.

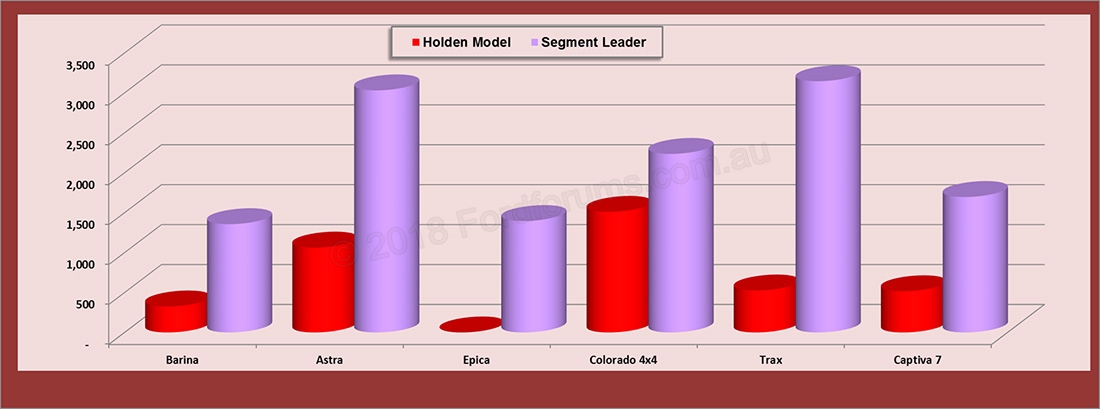

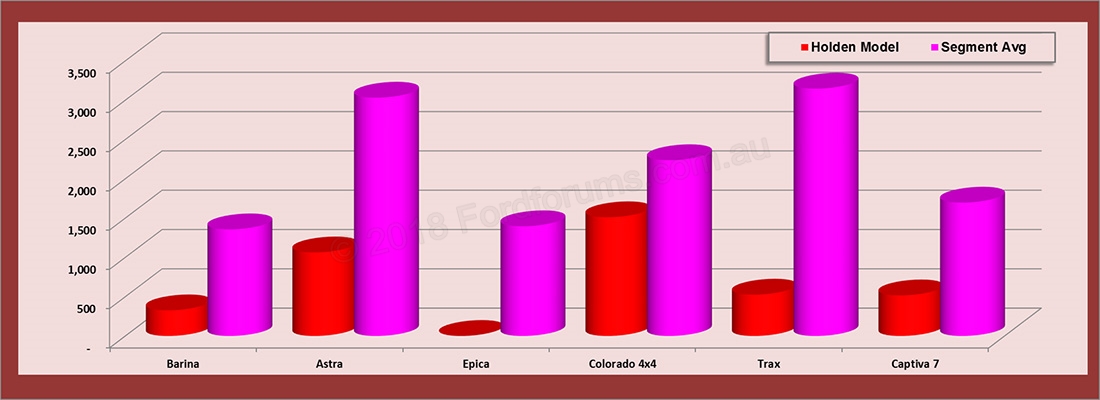

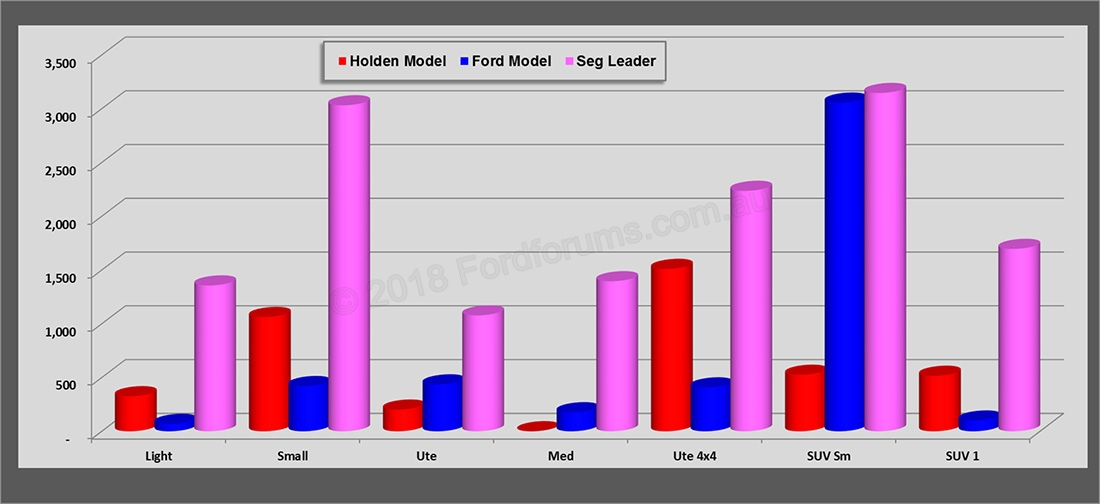

.. and a similar comparison for the Holden Models where Barina (down to 4.16), Astra (up to 2.85 ), Captiva 7 (up to 3.29), Trax (up to 5.99) and Colorado 4x4 (up to 1.48), Colorado 4x2 (up to 5.35) are all being outsold by the segment leaders with only the Commodore holding the lead in the large segment.

.. and finally the two combined.

Buyer Types

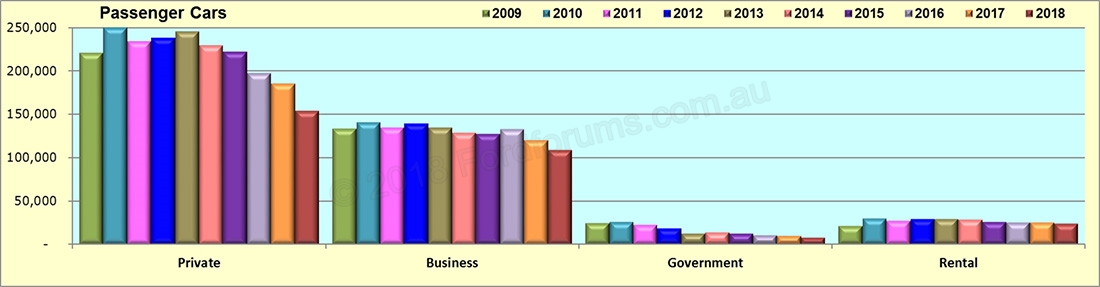

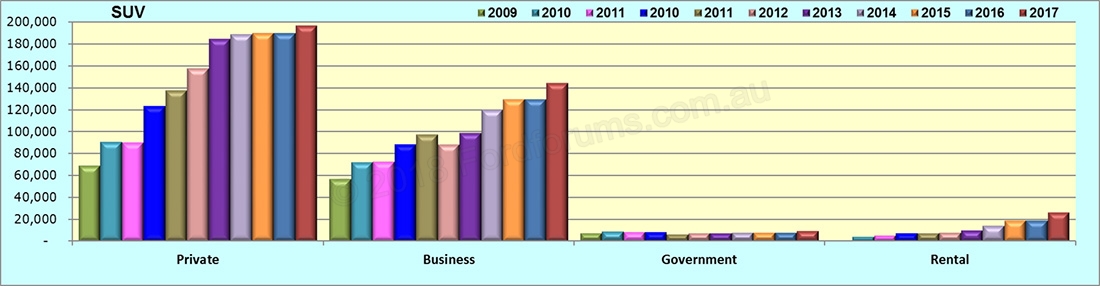

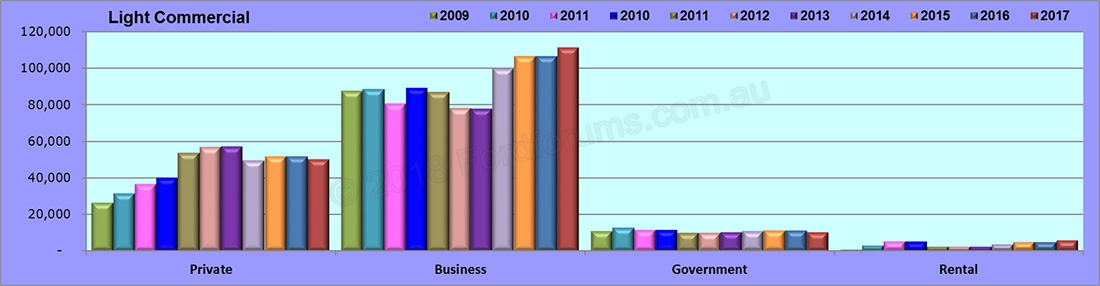

The raw data used for the charts below looks at sales of each type of vehicle across three broad segments by buyer classification and shows the buying trends across the period being reviewed.

The three charts below look at each segment graphically:

In the passenger segment, its all negative this year compared to 2017 with Private buyers down 16.76%, Business down 9.55%, Government purchases down 17.76% and Rental down 5.64%. All sectors are also down across the ten-year period with Government having the largest drop of 66.7% over that time and private buyers down 30.31% so passenger vehicle buyers have clearly not been contributing to the overall 10-year market growth and the segment continues to decline in real terms.

The SUV sector is all positive compared to last year: Private sales 3.54% up while Government (+20.59%), Business (+11.3%) and Rental (+49.58%) all show gains. All buyer types for SUV show an improvement over the ten-year trend emphasising the continued strength of this vehicle type with private buyers up 185.5% over that time, business up 155.05% and Rental up 1997%. As most of the improvements between 2008 and 2018 are above the total market growth this is clearly the strongest growth sector.

Finally, the light commercial segment has had a mixed result compared to 2017 with Rental up 20% and Business buyers up 4.25% while private sales are down 2.96% and Government down 8.92%. The ten-year trend shows 88.96% growth in private buyers indicating the move toward dual purpose vehicles (like the crew cab ute) but a 6.44% drop in the Government sector and gains for Business (+26.84%) and Rental (+478%) buyers.

We also look at the percentage share of each segment held by each buyer type to see if this confirms the longer-term trends.

In the passenger segment, private buyer share from 57.97% in 2013 to 52.22% this year; Government has dropped from 3.11% to 2.84% in the same period although it had been much higher a decade ago while Business buyers are up from 31.93% to 36.77% and Rental buyer share has risen from 6.99% to 8.17% over that same period.

In the SUV segment, the private buyer share has decreased since 2013 from 55.19% to 52.14%. Government share has dropped from 2.65% to 2.56%; Business share decreased from 39.12% to 38.27% and Rental share has increased significantly from 3.14% to 7.03%.

The trend differs in light commercials with private buyer share dropping sharply, from 34.98% in 2013 to 28.24% now while Business buyer share increased from 56.66% to 62.4% with the balance being taken up by a decrease in Government (6.59% to 5.9%) and an increase in Rental sales (1.77% to 3.46%).

Fuel Types

We also look at the type of fuel that is being used in the vehicles sold today and it comes as little surprise that there has been a significant upturn in the sale of diesel powered vehicles and a corresponding downturn in the sales of those powered by petrol although there appears to be a recent reversal in the overall trend.

Hybrid / Electric sales are starting to increase again although they still are much better than even a couple of years ago albeit statistically insignificant representing only 3.29% of the passenger market and 1.12% overall, both well up on last year.

Please note that we changed the calculation method for the percentage variations in April 2009 so they are not directly comparable with prior months. We have also included a second chart for each data set that shows the percentage share held by each fuel type in the segment as this is probably a more definitive way of looking at the data.

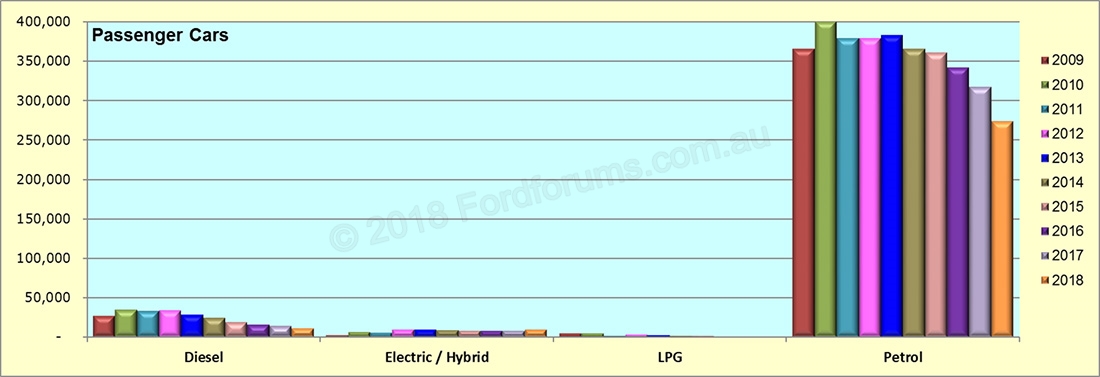

In the passenger car segment, we see a continued weakening in the demand for diesel powered vehicles and they are down by 20.86% for the year to date in a market that has only softened by 1.28% and they are now down 58.5% across the ten-year period. Youd expect this will only become a stronger trend although the reasons arent terribly clear.

There has been a 248.7% increase in hybrid / electric powered vehicles across the longer period and they are up by 15.31% this year in a reversal of the trend apparent in 2017. The trend for LPG also continues a downward spiral with the drop being almost total as the two locally manufactured offerings have left the market.

Sales of petrol powered vehicles are down by 13.81% for the year with the longer-term trend of 25.2% down over the ten-year period sending mixed messages about diesel use.

The percentage chart shows that hybrid / electric sales gained share to 3.12% of the passenger segment while LPG powered sales are almost non-existent and despite the massive increase in diesel vehicle sales over the last few years, they are still only 3.76% of passenger vehicle sales and slowly declining.

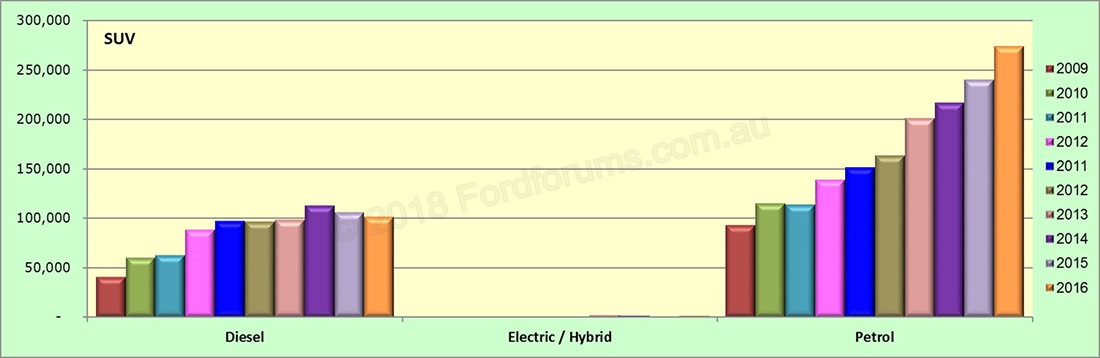

Similarly, sales of diesel powered SUVs have risen significantly over the ten-year period, being up 148.2% but they have also underperformed this year with the 3.93% drop being more significant because the segment itself grew overall. Hybrids have gained sales in this segment but a 18.56% increase this year only means 274 more have been sold. Petrol SUV sales are up 14.22% this year, while the ten-year trend is now showing a 195.1%gain so it appears the love affair with diesels is slowing in the more consumer oriented segments.

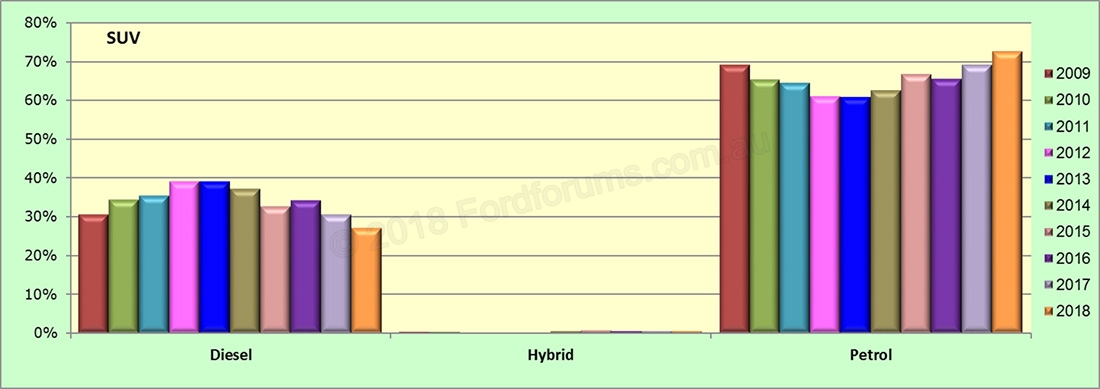

The percentage chart shows that diesel continues to decline in share but still holds more than a quarter of the segment (26.97%) although this is well down on the 33+ of 2017 while hybrids now make up 0.46% and petrol sales have grown market share to 72.56%.

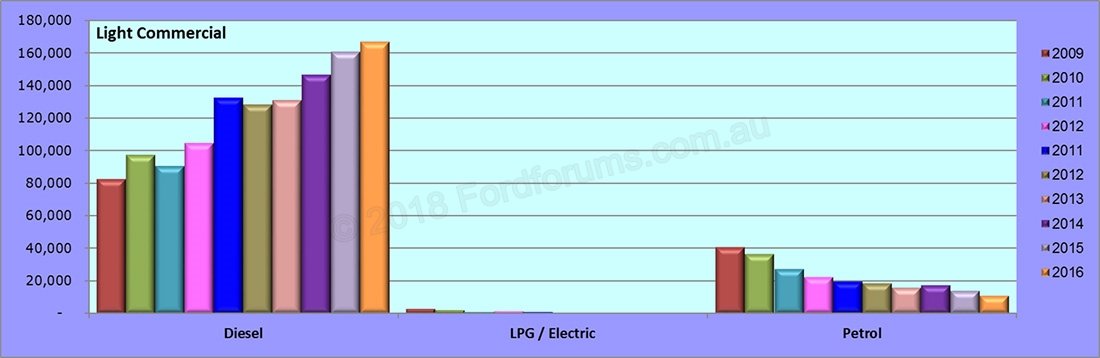

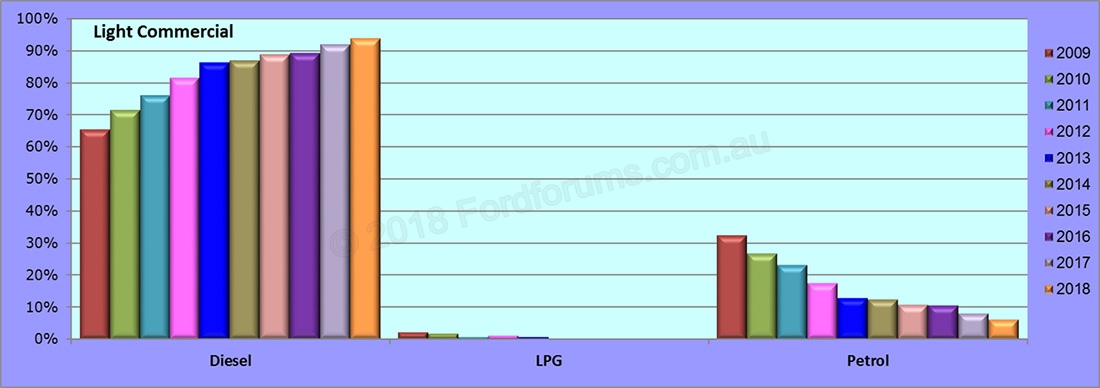

Light commercials show an increase in diesel sales for 2017, up 5.19% this year and they are up 98.5% over the ten years. LPG is pretty much non-existent and petrol sales are down 72.4% across the ten-year period and down 18.15% this year.

The percentage chart shows a further increase in the growth of diesel sales and they are now 93.58% of the segment - there has also been a sharp decrease in the penetration of petrol sales from 32.22% in 2009 to just 6.41% now.

We also take a longer term view of the changing consumer taste for vehicles. The data used goes back to 2000 so we end up with eighteen years under review - sufficient time for any statistical trends to become obvious.

Note: Some statistical categories have changed over this time but after reviewing the data it is my view that there is no significant impact on the validity of the data caused by those changes. We maintain our own categories that are slightly different from the FCAI ones anyway as a means of ensuring a level playing field for time series data and this has minimised the impact.

We are going to look at two sets of data:

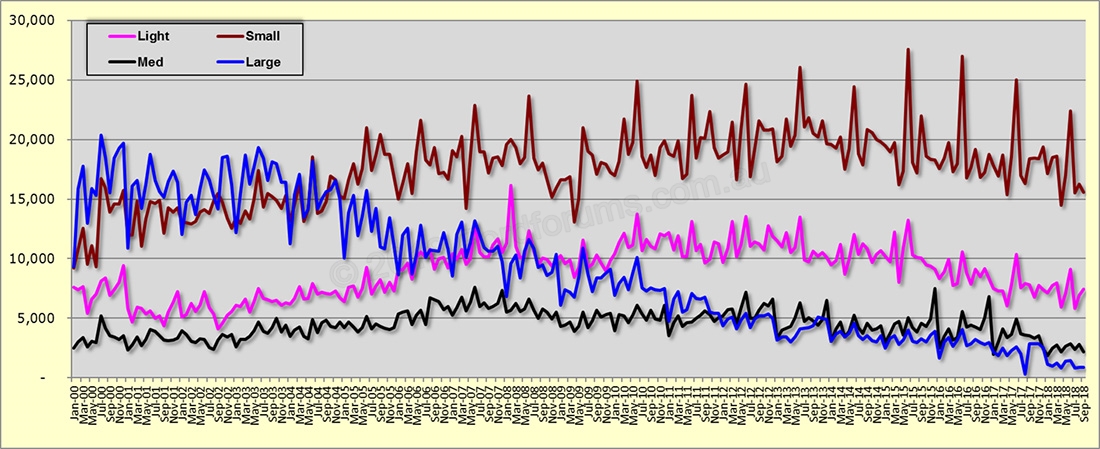

1. The four passenger car segments (light, small, medium and large). Here we can clearly see the growth in the small car segment, the massive slide of the large car segment and the growth of both the light and medium segments followed by a gradual decline in both.

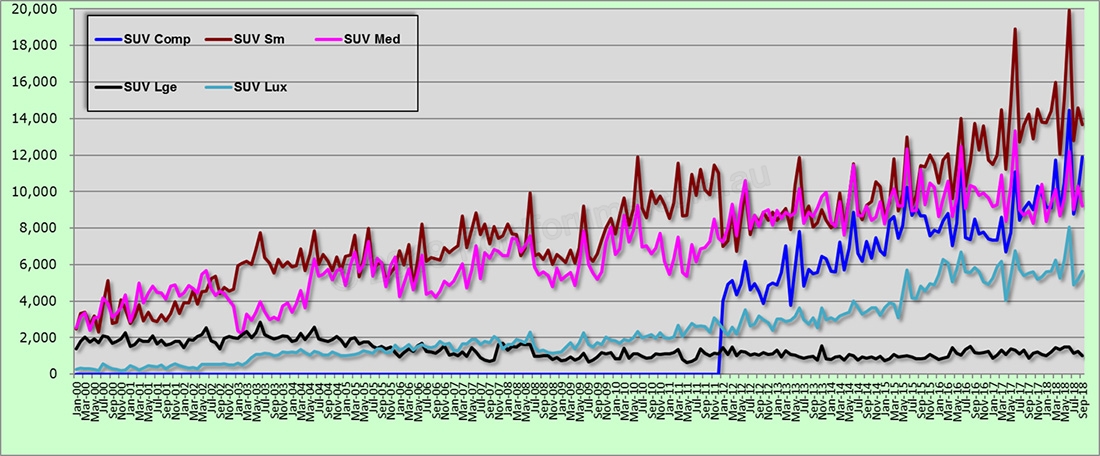

2. The five SUV segments (compact, small, medium, large and luxury) which continue to show a growth trend.

Model Performance

In these charts we are looking at the sales for the models represented in each segment by Ford, Holden and Toyota to take a look at their year on year and five year performance. Where models have changed (as in Avalon to Aurion) the figures for both are included.

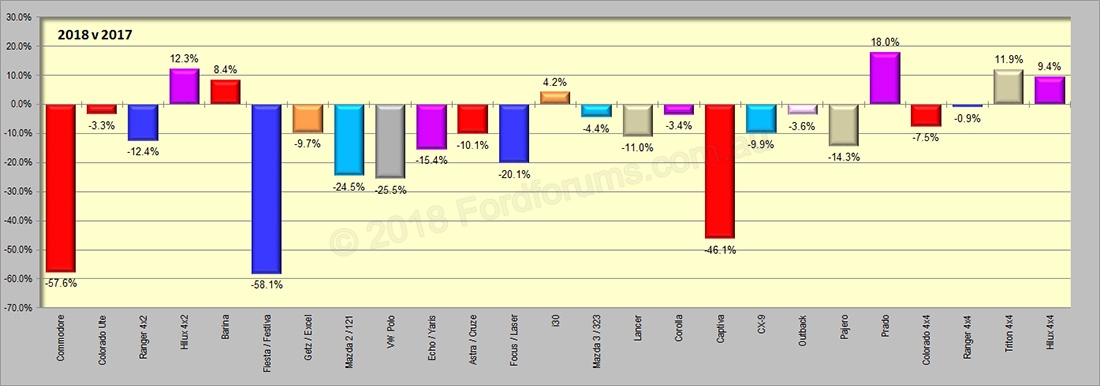

First up is the performance this year against last where the biggest winner is the Toyota Prado (+18%) and the biggest loser Ford Fiesta (-58.1%). Note that we have excluded all the models that became defunct last year.

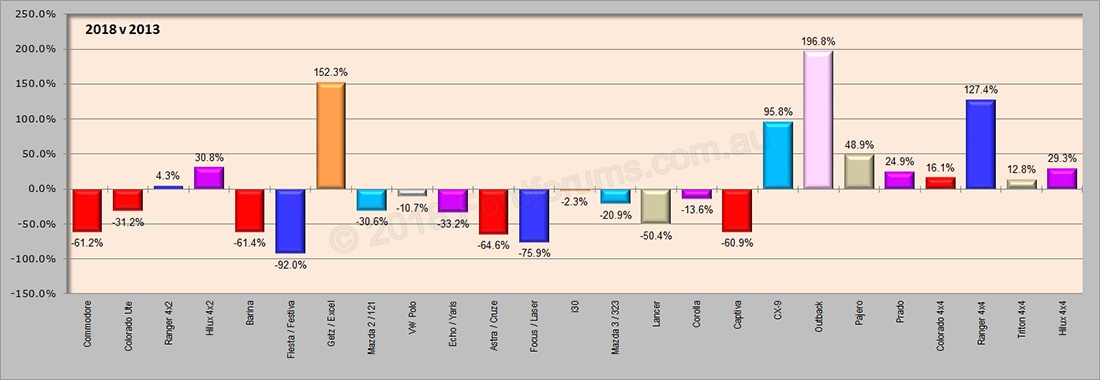

Next we look at the comparison between 2018 and 2013 (5 years) where the big winners are Ranger 4x4 up 127.4%; Hyundai Getz up 152.3% and the Subaru Outback up 196.8%. The Ford Fiesta tops the losing pack, down -92% just ahead of the Ford Focus which is down 75.9%.

The final chart in this series looks at each segment 2018 - 2012 in terms of their volume for the month. For the first time in a while we see a mixed bag of results between this and last year with most segments improving but some not.

Supplementary Sales Stats September 2018

Supplementary Sales Stats September 2018

Be The First